Sector - Finance & Legislation

Never mind the risk, it’s uncertainty management

Certainty leads to confidence. For large, complex and long duration projects and programmes, uncertainty is a limitation to achieving this confidence amongst stakeholders. Risks are a contributing factor to uncertainty and subsequent confidence, but they are only part of the bigger picture.

Risks are an estimate of known possible events. Stakeholder confidence is also influenced by the organisation’s ability and competency for identifying all other sources of uncertainty – not only risk events. Paying attention to planning and estimating assumptions is an equally important source of uncertainty, helping to determine which factors are most sensitive.

Traditional risk management

A traditional approach to risk management can have many benefits for project and programme delivery, enabling project managers to focus on and protect their performance and objectives. When implemented and prioritised effectively, the identification and subsequent management of threats and opportunities can promote a feeling of control and confidence within the project management team.

However, this approach can be very limiting. Purely focusing on threats and opportunities constrains the mind from considering all the possible uncertainties that may impact on the objectives of the project / programme.

Uncertainty in assumptions

Uncertainties may be difficult to quantify, they may be hard to visualise or may be out of the project/programme’s ability to control. It is, however, important to identify and scale them to determine what really matters and what needs further exploration.

Some of these uncertainties may have (either knowingly or not) been assumed to be fact in earlier stages of the project and have formed the entire basis of the project cost and schedule. As such, it is crucial that these assumptions are captured when estimating and appropriate consideration is made with respect to conditions, including but not limited to:

- Complexity

- Proximity

- Novelty

- Effort required

- Methodology

These assumptions may either be at an extreme end of an uncertainty scale (e.g. worst possible case or best possible case scenarios) but equally they may have been assumed at some point between these extreme values.

In a traditional risk management / analysis approach, a false assumption in the above scenario may be represented as a threat (if assumed a best-case scenario) or an opportunity (if assumed a worst-case scenario). However, the reality is that many estimating assumptions are at some point between a minimum possible value and a maximum possible value. In these cases, the assumptions should be represented with uncertainty estimates and modelled with appropriate distribution functions. Threats and opportunities should not be confused with uncertainty – they should address the key future chance “events”. Indeed, maintaining a modest risk register may be beneficial in the execution phase, since all too often risk registers can become unwieldy and it can become too easy to be bogged down in items that are of little or no significance.

Focus on the things that matter

The uncertainties associated with a project’s work scope and assumptions are equally as important as the traditional approach to risk management. It is important to ensure a holistic approach is taken – to ensure appropriate attention is paid to the things that matter. It may be more critical to further explore and better define a future area of uncertainty early in the project lifecycle, than to mitigate a near term risk.

Furthermore, it is important to pay attention to work scope proximity. Both the estimates or collection of estimates that are in the years ahead and the estimates in the very short term should be represented. The level of detail may not be known / explored for work in the future and may therefore represent a higher level of uncertainty. This is particularly relevant with planning and scheduling.

Think outside of the risk register box

There are tools and techniques to help understand and visualise relationships between uncertain variables. Causal loop diagrams can be of great help to build a system model of relationships between variables. There are many other underutilised tools and techniques that could be exploited by project risk management professionals.

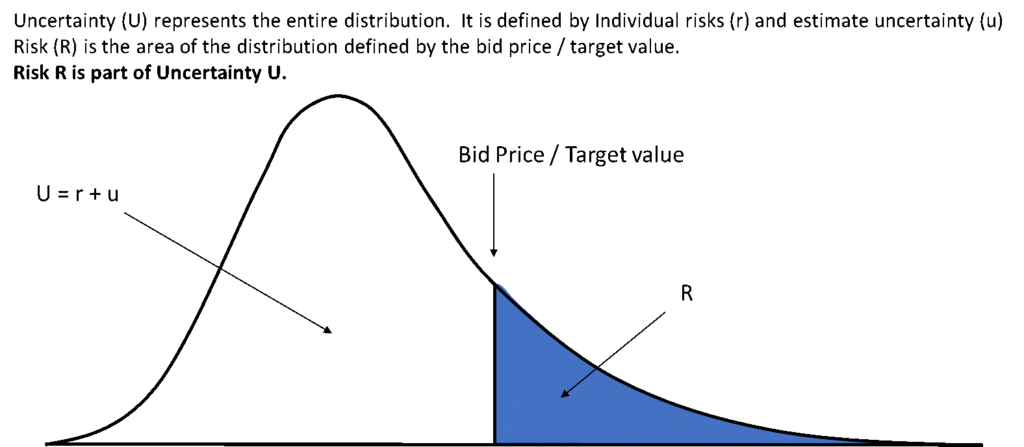

Uncertainty management

Risk management is a key part of uncertainty management. In the context of the diagram below, risk (R) is a measure of the committed value and the simulated values exceeding it. This can be measured on a regular basis throughout a project’s execution by conducting Monte Carlo analysis of a Project that includes both risks and uncertainty.

The term “risk management” has become associated with events rather than generic sources of uncertainty. This limited focus restricts project management improvement and performance.

Perhaps risk management needs a new name. Uncertainty management far better expands the possibilities of discovery and supports prioritisation and focus on the things that matter.

The full context of risk can only be measured when threats, opportunities AND uncertainties have been explored and quantified in a model.

Mark Matthew is a principal risk manager at risk management consultancy, Equib, which specialises in advising teams involved in the delivery of major-scale infrastructure programmes.

If you would like to read more stories like this, then please click here

More Finance & Legislation Features

- Britain’s Builders Are Waiting 53 days to Get Paid, and Eight in Ten Are Eight Months from Collapse

24 Jun 26

Britain's construction sector is heading for a cashflow crisis.

- The Return of CIS NIL Returns and Key Changes for Contractors in 2026

17 Jun 26

Alex Seal from Markel Tax discusses the reintroduction of CIS NIL return requirements from April 202.

- One in five builders say late payments threaten their business

1 May 26

Cashflow pressures remain a major challenge for self-employed construction and building workers, according to new research.